Refinancing a mortgage can help some homeowners lower monthly payments, change loan terms, remove mortgage insurance, switch from an adjustable-rate mortgage to a fixed-rate mortgage, or access home equity through a cash-out refinance.

But refinancing is not always the right move.

A lower rate can look attractive, but refinance closing costs, loan term changes, lender fees, appraisal charges, title costs, credit score, home equity, and the break-even point all matter.

Freddie Mac explains that refinance closing costs often range from 3% to 6% of the loan principal, depending on lender, credit score, and location. (My Home) Fannie Mae says refinancing typically costs between 2% and 5% of the new loan amount, and those fees may be paid upfront or rolled into the new loan depending on the loan. (Fannie Mae)

That means refinancing a $300,000 mortgage may involve thousands of dollars in costs. If the monthly savings are small or you plan to move soon, the refinance may not be worth it.

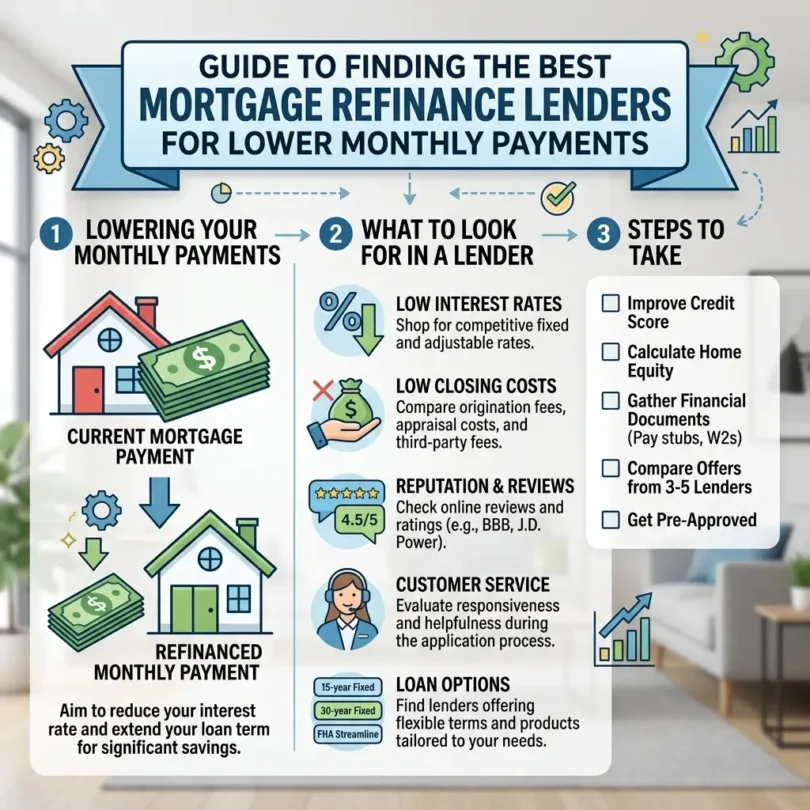

This guide explains how to compare the best mortgage refinance lenders, what refinance options exist, which lender types to consider, how closing costs work, how to calculate the break-even point, and what mistakes to avoid before signing a new mortgage.

Important Disclaimer

This article is for general informational purposes only. It is not legal, tax, mortgage, real estate, lending, or professional advice.

Mortgage rates, lender fees, refinance eligibility, credit rules, closing costs, state laws, and loan terms change often. Always compare official Loan Estimates from multiple lenders and speak with a licensed mortgage professional, attorney, tax professional, or housing counselor before making a refinance decision.

What Is Mortgage Refinancing?

Mortgage refinancing means replacing your current home loan with a new mortgage.

The new loan pays off the old loan. After closing, you make payments on the new mortgage instead of the old one.

Homeowners usually refinance to:

- Lower monthly payment

- Reduce interest rate

- Change loan term

- Switch from adjustable rate to fixed rate

- Remove private mortgage insurance

- Access home equity with cash-out refinance

- Combine first and second mortgage, if eligible

- Change loan type

- Add or remove a borrower

- Improve long-term loan structure

Refinancing can help, but it can also increase total cost if you extend the loan too long or roll large fees into the new balance.

Best Mortgage Refinance Lenders to Compare

The best mortgage refinance lender depends on your credit profile, home equity, loan type, property location, income documentation, debt-to-income ratio, existing mortgage, and refinance goal.

Below are lender types and companies commonly compared by homeowners.

1. Chase Home Lending

Best for: Homeowners who prefer a major bank with branch access

Good for: Existing Chase customers, conventional refinance, jumbo loans

Main strength: Large bank support and broad mortgage products

Chase is frequently included in mortgage lender comparisons. Bankrate’s 2026 refinance lender list included Chase among its best mortgage refinance lenders. (Bankrate)

Key Features to Compare

- Rate-and-term refinance

- Cash-out refinance

- Fixed-rate loans

- Adjustable-rate loans

- Jumbo loan options

- Online tools

- Branch support

- Existing customer relationship benefits, where available

Why Chase May Be Good

Chase may fit homeowners who prefer a well-known bank, in-person support, and broad loan options.

Possible Downsides

Large banks are not always the lowest-cost option. Compare official Loan Estimates from Chase, online lenders, credit unions, and mortgage brokers before deciding.

2. PNC Bank

Best for: Borrowers comparing bank-based refinance options

Good for: Conventional loans, government-backed refinance options, online and branch support

Main strength: Broad lending footprint

PNC Bank was also included in Bankrate’s 2026 list of best mortgage refinance lenders. (Bankrate)

Key Features to Compare

- Fixed-rate refinance

- Adjustable-rate refinance

- Cash-out refinance

- FHA and VA options, depending on eligibility

- Online application tools

- Branch support in many areas

- Mortgage calculators

Why PNC May Be Good

PNC may be useful for homeowners who want a traditional lender with digital tools and physical branch support.

Possible Downsides

Rates and lender credits can vary by borrower and location. Always compare more than one lender.

3. Pennymac

Best for: Homeowners wanting a mortgage-focused lender

Good for: Rate reduction, cash-out refinance, FHA/VA refinance options

Main strength: Dedicated mortgage lending platform

Pennymac is a major mortgage lender and was included in Bankrate’s 2026 refinance lender list. (Bankrate) Pennymac’s refinance page says homeowners can explore options to lower payments, reduce rates, or access equity. (Pennymac)

Key Features to Compare

- Rate-and-term refinance

- Cash-out refinance

- FHA refinance

- VA refinance

- Online application

- Mortgage calculators

- Servicing experience

- Loan officer support

Why Pennymac May Be Good

Pennymac may fit borrowers who want a lender focused heavily on mortgages rather than a full-service bank.

Possible Downsides

Customer service experience can vary. Compare lender fees, reviews, and closing timelines before choosing.

4. Better Mortgage

Best for: Digital refinance experience

Good for: Online-first borrowers, quick quote comparison, no-branch shoppers

Main strength: Technology-driven mortgage process

Better was included in Bankrate’s broader 2026 best mortgage lender list. (Bankrate) Digital lenders can be useful for borrowers who want online quotes and a faster application workflow.

Key Features to Compare

- Online preapproval

- Digital document upload

- Rate-and-term refinance

- Cash-out refinance, where available

- Transparent online process

- Fast application workflow

- No in-person branch requirement

Why Better May Be Good

Better may fit homeowners who prefer a digital experience and want to compare quotes without visiting a branch.

Possible Downsides

Online lenders may not be ideal for borrowers who want in-person help or have complex income documentation.

5. Rocket Mortgage

Best for: Digital mortgage process and broad brand recognition

Good for: Online applicants, conventional refinance, FHA/VA refinance where eligible

Main strength: Large online mortgage platform

Rocket Mortgage is one of the most recognized online mortgage lenders. NerdWallet’s 2026 awards named Rocket Mortgage as a top first-time homebuyer lender, showing the brand’s broad presence in mortgage comparisons. (Morningstar)

Key Features to Compare

- Online refinance application

- Conventional refinance

- FHA refinance

- VA refinance, where eligible

- Cash-out options

- Rate lock options

- Digital document process

- Large mortgage support team

Why Rocket Mortgage May Be Good

Rocket Mortgage may fit borrowers who want a polished online process and a well-known mortgage brand.

Possible Downsides

Convenience does not always mean lowest cost. Compare Loan Estimates from multiple lenders.

6. Wells Fargo

Best for: Existing Wells Fargo customers and bank-based mortgage support

Good for: Traditional bank refinance, jumbo options, branch access

Main strength: Large national banking network

Wells Fargo appeared in Bankrate’s 2026 best mortgage lenders list and refinance lender list. (Bankrate)

Key Features to Compare

- Conventional refinance

- Jumbo refinance

- Cash-out refinance

- Fixed-rate loans

- Adjustable-rate loans

- Branch and phone support

- Existing customer support

Why Wells Fargo May Be Good

Wells Fargo may be useful for homeowners who prefer a major bank and already have a relationship with the company.

Possible Downsides

Major banks may have more documentation steps. Compare speed, fees, and rates.

7. PenFed Credit Union

Best for: Credit union refinance options

Good for: Members, competitive rate shoppers, eligible borrowers

Main strength: Credit union structure and mortgage options

PenFed Credit Union was included in Bankrate’s 2026 refinance lender list. (Bankrate)

Key Features to Compare

- Conventional refinance

- VA refinance for eligible borrowers

- Jumbo loan options

- Credit union membership

- Online application

- Rate comparison tools

- Member-focused support

Why PenFed May Be Good

Credit unions can sometimes offer competitive pricing and member-focused service. PenFed may be worth comparing if you are eligible for membership.

Possible Downsides

Membership rules and product availability should be reviewed before applying.

8. Navy Federal Credit Union

Best for: Eligible military households

Good for: VA refinance, military families, veterans, eligible members

Main strength: Military-focused lending

Navy Federal appeared in Bankrate’s 2026 first-time homebuyer lender comparison and is often compared by eligible military families for mortgage products. (Bankrate)

Key Features to Compare

- VA refinance options

- Conventional refinance

- Military-focused service

- Credit union membership

- Online tools

- Member support

- Possible no-down-payment products for purchase loans, where eligible

Why Navy Federal May Be Good

Navy Federal may be strong for eligible military members, veterans, and family members who want a lender familiar with military borrower needs.

Possible Downsides

Not everyone qualifies for membership. Always compare VA refinance offers with multiple lenders.

9. NBKC Bank

Best for: Online refinance and customer service reputation

Good for: Digital borrowers, VA and conventional borrowers, online process

Main strength: Online application and service reputation

Bankrate’s NBKC Bank mortgage review said NBKC may be good for borrowers looking for an entirely online application process, fast preapproval, and excellent customer service. (Bankrate)

Key Features to Compare

- Online application

- Conventional refinance

- VA loan options

- Fast preapproval

- Digital process

- Customer service reputation

- Competitive pricing, depending on borrower profile

Why NBKC May Be Good

NBKC may fit borrowers who want an online-first experience but still care about service quality.

Possible Downsides

Product availability and pricing may vary by state and borrower profile.

10. Local Credit Unions and Mortgage Brokers

Best for: Personalized comparison and local market knowledge

Good for: Borrowers who want multiple lender options

Main strength: Local service and rate shopping support

Not every strong refinance option comes from a national brand.

Local credit unions, community banks, and mortgage brokers may offer competitive refinance options.

Key Features to Compare

- Local lender access

- Broker comparison across multiple lenders

- Credit union member pricing

- Personalized guidance

- Local closing support

- Conventional, FHA, VA, jumbo, and cash-out options

- Flexible support for unique borrower situations

Why Local Options May Be Good

A local credit union may offer strong pricing for members. A mortgage broker may compare multiple lender options at once.

Possible Downsides

Broker fees, lender fees, and available loan products vary. Ask clearly how the broker is paid and compare official Loan Estimates.

Quick Comparison Table

| Lender | Best For | Main Strength | Good Fit |

|---|---|---|---|

| Chase | Major bank support | Branch access and broad products | Existing bank customers |

| PNC Bank | Bank-based refinance | Digital plus branch support | Traditional borrowers |

| Pennymac | Mortgage-focused lending | Refinance options and servicing | Homeowners comparing rates |

| Better | Digital process | Online-first application | Tech-friendly borrowers |

| Rocket Mortgage | Online mortgage experience | Large digital platform | Fast online shoppers |

| Wells Fargo | Major bank refinance | Broad mortgage presence | Existing bank customers |

| PenFed | Credit union refinance | Member-focused pricing | Eligible credit union members |

| Navy Federal | Military households | VA-focused support | Eligible military families |

| NBKC Bank | Online service | Fast preapproval and service | Digital borrowers |

| Local brokers/credit unions | Personalized comparison | Multiple local options | Rate shoppers |

Main Types of Mortgage Refinance

1. Rate-and-Term Refinance

A rate-and-term refinance changes your interest rate, loan term, or both.

Homeowners often use it to:

- Lower monthly payment

- Reduce rate

- Change from 30-year to 15-year loan

- Change from adjustable to fixed rate

- Remove mortgage insurance if eligible

This is one of the most common refinance types.

2. Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a larger new mortgage. The difference is paid to you in cash at closing.

Homeowners may use cash-out refinance for:

- Home improvements

- Debt payoff

- Emergency needs

- Large expenses

- Investment in property repairs

Warning

Cash-out refinance increases the loan balance and uses your home as collateral. If payments become unaffordable, the home can be at risk.

3. Streamline Refinance

Some government-backed loans may offer streamline refinance options.

Examples may include:

- FHA streamline refinance

- VA Interest Rate Reduction Refinance Loan

- USDA streamline options, where eligible

These may have simpler documentation rules, but eligibility requirements apply.

4. No-Closing-Cost Refinance

A no-closing-cost refinance does not mean there are no costs.

Usually, the lender either:

- Rolls costs into the loan balance, or

- Charges a higher rate in exchange for covering some costs

This may help reduce upfront cash needed, but it can increase long-term cost.

5. Shorter-Term Refinance

Some homeowners refinance from a 30-year loan to a 15-year or 20-year loan.

This may help pay off the home faster and reduce total interest, but monthly payments may increase.

When Does Refinancing Make Sense?

Refinancing may make sense if:

- You can get a lower interest rate

- Monthly savings outweigh closing costs

- You plan to stay in the home past the break-even point

- You want to switch from adjustable to fixed rate

- You can remove mortgage insurance

- You need to change loan term

- You qualify for better terms

- You need cash-out and understand the risk

- You can improve long-term loan structure

WSJ Buy Side reported that 30-year fixed mortgage rates averaged around the mid-6% range in June 2026, and that homeowners with loans above current rates may benefit from refinancing if long-term savings outweigh costs. (Wall Street Journal)

When Refinancing May Not Make Sense

Refinancing may not be right if:

- Closing costs are too high

- You plan to sell soon

- Your current rate is already low

- Your credit score has dropped

- You have low home equity

- You will restart a 30-year term and pay more over time

- You cannot afford closing costs

- You are using cash-out for short-term spending

- The new loan has risky terms

- You do not understand the break-even point

A refinance should improve your situation, not only lower the monthly payment while increasing total cost too much.

How to Calculate the Refinance Break-Even Point

The break-even point shows how long it takes for monthly savings to recover refinance costs.

Simple formula:

Refinance closing costs ÷ monthly payment savings = months to break even

Example:

- Closing costs: $5,000

- Monthly savings: $250

- Break-even point: 20 months

If you plan to stay in the home longer than 20 months, the refinance may be worth considering. If you plan to sell in 12 months, it may not be worth it.

Freddie Mac offers a refinance calculator that estimates monthly savings, total interest savings, and break-even point. (My Home)

Refinance Closing Costs: What to Expect

Refinance closing costs may include:

- Loan origination fee

- Application fee

- Appraisal fee

- Credit report fee

- Title search

- Title insurance

- Recording fees

- Attorney fees, in some states

- Escrow or settlement fees

- Prepaid taxes and insurance

- Discount points

- Flood certification

- Government fees

Freddie Mac says refinance costs can include lender fees and other closing costs, and homeowners can expect to spend about 3% to 6% of loan principal. (My Home)

How to Compare Mortgage Refinance Lenders

1. Compare Loan Estimates

A Loan Estimate is one of the most important refinance documents.

CFPB provides a Loan Estimate explainer to help borrowers review whether the document reflects what they discussed with the lender. (Consumer Financial Protection Bureau) CFPB also advises borrowers to review Loan Estimates to compare costs and loan risk between offers. (Consumer Financial Protection Bureau)

Compare:

- Interest rate

- APR

- Monthly principal and interest

- Closing costs

- Discount points

- Lender credits

- Prepayment penalty, if any

- Estimated cash to close

- Loan term

- Adjustable-rate features, if any

2. Compare APR, Not Only Interest Rate

The interest rate affects monthly payment, but APR includes more loan costs.

A lower interest rate with high fees may not be better than a slightly higher rate with lower costs.

3. Ask About Points

Discount points are upfront costs paid to lower the interest rate.

Ask:

- How much does each point cost?

- How much does it reduce the rate?

- What is the break-even point?

- Will I stay in the home long enough?

4. Compare Closing Costs

Two lenders may offer the same rate but very different costs.

5. Check Closing Timeline

If you need fast closing, ask:

- How long does refinance usually take?

- Is appraisal required?

- How fast can underwriting review documents?

- Are there known delays?

6. Review Customer Service

A low rate can become stressful if the lender is slow, confusing, or disorganized.

7. Ask About Servicing

Some lenders sell servicing after closing. Ask who will collect payments after the refinance.

What Credit Score Do You Need to Refinance?

Credit score requirements vary by lender and loan type.

In general:

- Higher scores usually qualify for better rates

- Lower scores may still qualify through FHA or other programs

- Credit history, payment history, debt-to-income ratio, income, and home equity also matter

- Lenders may have overlays beyond program minimums

Before applying, review your credit reports and fix errors if possible.

What Documents Do You Need to Refinance?

Lenders may request:

- Government ID

- Recent pay stubs

- W-2 forms

- Tax returns, especially for self-employed borrowers

- Bank statements

- Current mortgage statement

- Homeowners insurance

- Property tax information

- HOA information, if applicable

- Credit authorization

- Asset documents

- Business documents, if self-employed

- Divorce decree or support documents, if relevant

- Explanation letters, if needed

Having documents ready can speed up the process.

Best Refinance Lender by Borrower Type

Best for Online Borrowers

Compare:

- Better

- Rocket Mortgage

- NBKC Bank

- Pennymac

Best for Major Bank Customers

Compare:

- Chase

- PNC Bank

- Wells Fargo

Best for Credit Union Members

Compare:

- PenFed

- Navy Federal, if eligible

- Local credit unions

Best for Military Households

Compare:

- Navy Federal

- PenFed

- Veterans United, where relevant

- Other VA-approved lenders

Best for Cash-Out Refinance

Compare lenders based on:

- Maximum loan-to-value

- Rate

- Fees

- Closing costs

- Cash-out rules

- Underwriting speed

- Home equity requirements

Best for Low-Cost Refinance

Compare:

- Credit unions

- Online lenders

- Mortgage brokers

- Major lenders with lender credits

- Local banks

Mortgage Refinance Scams to Avoid

Mortgage-related scams are common, especially when homeowners are under stress.

The FTC warns that mortgage relief scammers may falsely claim they can negotiate with your lender or servicer for a fee, often paid upfront, and may pretend to be connected to government housing assistance programs. (Federal Trade Commission)

Avoid anyone who:

- Demands upfront fees for mortgage relief

- Guarantees lower payments

- Tells you to stop talking to your lender

- Claims government affiliation without proof

- Tells you to transfer your deed

- Pressures you to sign quickly

- Promises to stop foreclosure for a fee

- Tells you to make payments to them instead of your lender

- Refuses to provide written terms

- Uses fear tactics

The FTC says scammers may promise they can stop foreclosure if you pay them, but no one can guarantee that. (Consumer Advice)

Common Mortgage Refinance Mistakes

Mistake 1: Focusing Only on Monthly Payment

A lower payment may come from extending the loan term, not only lowering the rate.

Mistake 2: Ignoring Closing Costs

Refinancing is not free. Always calculate break-even.

Mistake 3: Not Comparing Multiple Lenders

One lender’s offer may be much higher than another’s.

Mistake 4: Not Reviewing Loan Estimate

Read the Loan Estimate carefully before moving forward.

Mistake 5: Rolling Costs Into the Loan Without Thinking

This may reduce upfront cash but increase the loan balance.

Mistake 6: Resetting to a 30-Year Loan Too Often

Repeated refinancing can keep you paying for longer.

Mistake 7: Using Cash-Out Refinance Carelessly

Cash-out refinance increases mortgage debt and puts home equity at risk.

Mistake 8: Not Checking Credit First

Credit errors can lead to worse terms.

Mistake 9: Paying for Points Without Calculating Break-Even

Points only make sense if you stay long enough to benefit.

Mistake 10: Trusting Guaranteed Claims

No lender can promise approval or savings without reviewing your full profile.

Refinance Checklist Before Applying

Before applying, check:

- Current mortgage rate

- Current loan balance

- Remaining loan term

- Estimated home value

- Home equity

- Credit score

- Debt-to-income ratio

- Monthly payment goal

- Break-even point

- Closing cost estimate

- How long you plan to stay

- Cash-out need, if any

- Mortgage insurance status

- Loan Estimate from multiple lenders

- Whether the new loan improves your situation

Final Verdict: What Are the Best Mortgage Refinance Lenders?

The best mortgage refinance lender depends on your goals, credit profile, home equity, location, and preferred application style.

For many homeowners:

- Best major bank options: Chase, PNC Bank, Wells Fargo

- Best mortgage-focused lender: Pennymac

- Best digital options: Better, Rocket Mortgage, NBKC Bank

- Best credit union options: PenFed, Navy Federal, local credit unions

- Best personalized comparison: Mortgage brokers and local lenders

Bankrate’s 2026 refinance lender list included Chase, PNC Bank, Wells Fargo, PenFed, Pennymac, and other lenders among refinance options to compare. (Bankrate)

Before choosing, compare official Loan Estimates from at least three lenders. Look beyond the interest rate. Compare APR, lender fees, points, credits, closing costs, monthly payment, break-even point, and long-term loan cost.

Refinancing can be helpful, but only when the savings, stability, or loan benefits outweigh the cost.

FAQs About Mortgage Refinance Lenders

What is mortgage refinancing?

Mortgage refinancing means replacing your current home loan with a new mortgage. The new loan pays off the old one, and you make payments on the new loan.

Who are the best mortgage refinance lenders?

Common lenders to compare include Chase, PNC Bank, Pennymac, Better, Rocket Mortgage, Wells Fargo, PenFed, Navy Federal, NBKC Bank, local credit unions, and mortgage brokers.

How much does it cost to refinance a mortgage?

Freddie Mac says refinance closing costs often range from 3% to 6% of the loan principal. (My Home) Fannie Mae says refinancing typically costs between 2% and 5% of the new loan amount. (Fannie Mae)

What is a refinance break-even point?

The break-even point is how long it takes monthly savings to recover refinance closing costs. Divide closing costs by monthly savings to estimate the break-even time.

Should I refinance to lower my monthly payment?

It may make sense if the monthly savings outweigh closing costs and you plan to stay in the home past the break-even point. It may not make sense if fees are high or you plan to move soon.

What is a cash-out refinance?

A cash-out refinance replaces your mortgage with a larger new loan and gives you the difference in cash. It increases the loan balance and uses your home as collateral.

What is a Loan Estimate?

A Loan Estimate is a document that helps borrowers compare mortgage offers. CFPB provides tools to help borrowers review and compare Loan Estimates. (Consumer Financial Protection Bureau)

Is no-closing-cost refinance really free?

No. Costs are usually rolled into the loan or covered through a higher rate. Always compare the total cost.

Can refinancing remove mortgage insurance?

Sometimes. If your home equity is high enough and lender rules allow it, refinancing may remove mortgage insurance. FHA mortgage insurance rules can differ.

How many refinance lenders should I compare?

Compare at least three lenders. More quotes can help you find a better rate, lower fees, or a stronger overall offer.